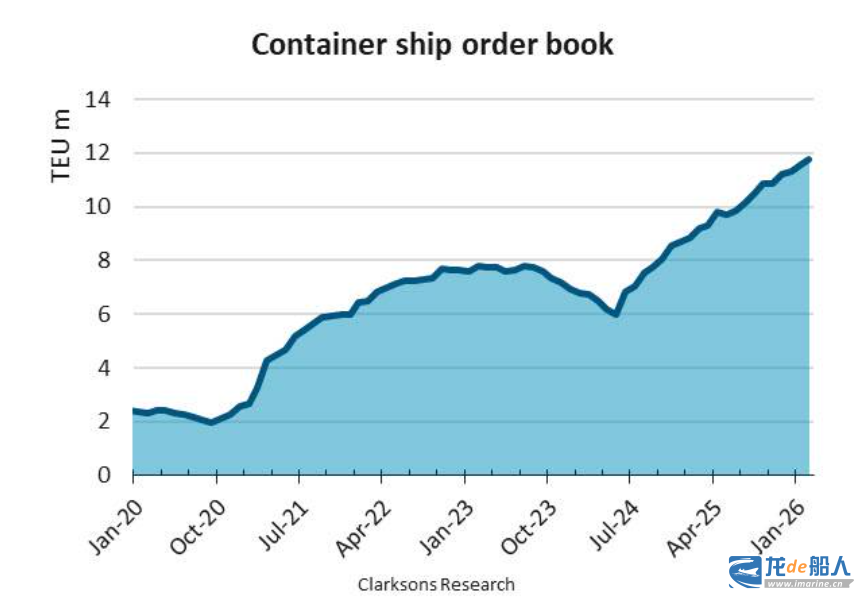

Despite heightened trade policy uncertainties and persistently falling freight rates, container ship orders continue to climb. Niels Rasmussen, Chief Shipping Analyst at the Baltic International Maritime Council (BIMCO), noted that the global container ship order book has now surpassed 1,350 vessels, with total capacity reaching 11.8 million TEU.

In 2025, global average container freight rates are expected to fall by approximately 13% year-on-year, with increased US import tariffs exacerbating concerns about rising trade protectionism. However, according to data from the Container Trade Statistics, global container throughput is still expected to increase by 4.7% year-on-year, and shipowners’ new ship orders have reached a record high of 4.8 million TEUs.

In the first two months of 2026, shipowners placed orders for another 102 container ships, with a total capacity of 665,000 TEU; as of the end of February, the total global container ship order volume reached 11.8 million TEU, a year-on-year increase of 28%.

Niels Rasmussen points out: “The dominance of ultra-large container ships in total orders indicates a trend of large vessels gradually replacing small vessels in the global shipping network. Currently, the 436 vessels with a capacity of 12,000 TEU and above under construction account for 65% of the total orders.”

Despite this trend, the fastest growth in orders over the past year has been for small container ships. Orders for the 0–3000TEU, 3000–6000TEU, and 6000–8000TEU segments have all more than doubled in the past year, while orders for other ship types have only increased by 17%.

However, the combined orders for these three segments only represent 16% of the existing fleet capacity. Given that 29% of the capacity in these three segments is currently provided by vessels 20 years and older, the number of older ships being scrapped in the coming years may equal or even exceed the number of new ship deliveries.

With the increasing number of orders for ultra-large container ships, the ownership structure of the container ship fleet is undergoing a major transformation.

In the early 2020s, non-operating shipowners (chartering companies) controlled 43% of the fleet’s capacity. This proportion has since fallen to 36% and will continue to decline—as non-operating shipowners account for only 24% of the capacity in the under-construction fleet.

Niels Rasmussen stated: “Between 2025 and 2029, the total capacity of container ships scheduled for delivery will reach 11.8 million TEU. Even if all vessels currently in service that are 22 years old or older are scrapped by the end of 2030, the fleet size will still maintain the average annual growth rate of 6.1% seen this decade. This could create a rather challenging supply-demand management environment for liner operators.”