Recently, at its annual seminar, shipbroker Howe Robinson Partners noted that approximately 280 bulk carriers are currently trapped within the Persian Gulf, with another 100 anchored outside the Gulf. This represents roughly 3.6%, 3%, and 2.2% of the global Panamax, Supramax, and Handymax bulk carrier fleets, respectively.

In 2025, the Persian Gulf accounted for approximately 4.3% of global dry bulk shipping trade volume. Within this, inbound cargo shipments represented 2.6% of the world’s total ton-miles, while outbound cargo shipments accounted for 1.7%.

Guy Hindley, Managing Partner of Dry Bulk and Projects at Howe Robinson, points out that the Strait of Hormuz remains a crucial waterway for seaborne fertilizer products and raw materials. The Persian Gulf region accounts for 72% of global limestone exports, 57% of sulfur shipments, 5% of global grain imports, and 2% of iron ore shipments.

Orders for Capesize bulk carriers rebound, with overall order volume hitting a 10-year high.

Janina Lam, dry bulk project analyst at Howe Robinson, noted that one of the key findings from their annual seminar was the positive momentum in the Capesize bulk carrier market, which has underpinned order growth in recent months. Data shows that from January to March 2026, Capesize bulk carrier orders increased by 24% in terms of deadweight tonnage.

In terms of deliveries, 44 Capesize bulk carriers (8.8 million deadweight tons) are scheduled for delivery in 2026, up from 36 vessels (7.2 million deadweight tons) in 2025. Projections indicate that Capesize bulk carrier deliveries will surge to 79 vessels (15.6 million deadweight tons) in 2027 and reach 82 vessels (16.9 million deadweight tons) in 2028.

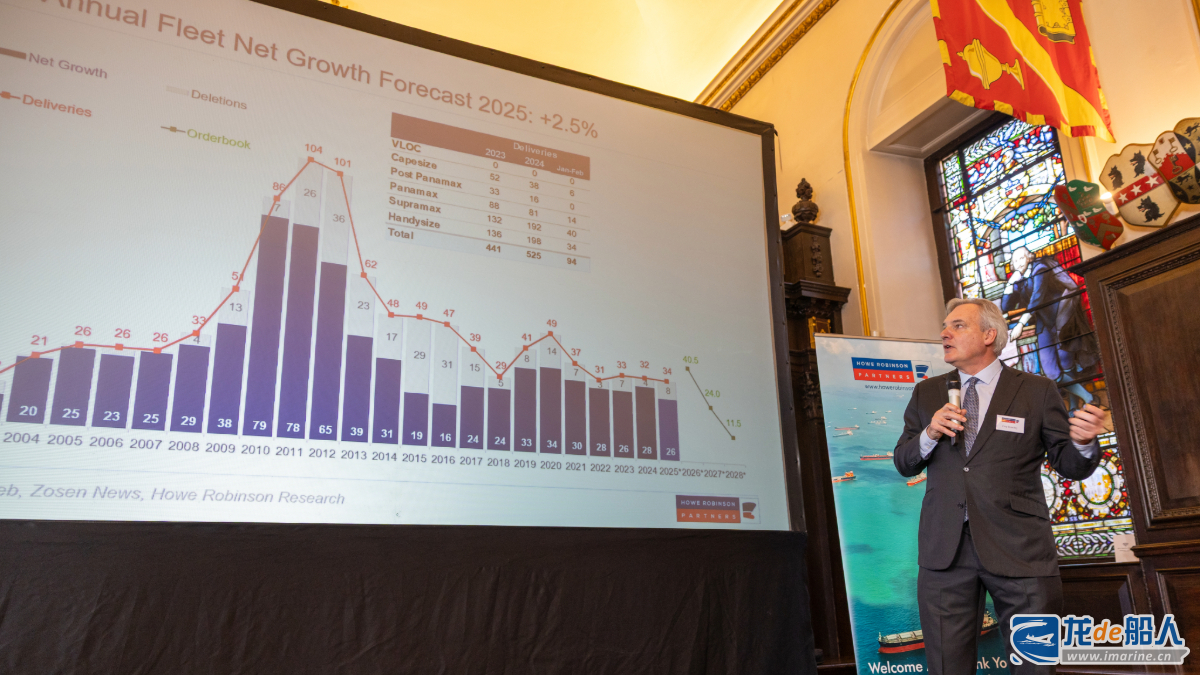

Overall, dry bulk carrier orders have reached a 10-year high, with current orders on hand totaling 1,618 vessels and a combined deadweight capacity of 142.2 million tons. Although new orders for 2025 remain below 2023 and 2024 levels, the current order volume represents approximately 13.3% of the active fleet. Meanwhile, bulk carrier capacity with vessels aged 20 to 30 years or older stands at 127.2 million deadweight tons. However, ship dismantling activities remain relatively limited, with shipowners generally opting to continue operating aging vessels or reselling them for trade rather than sending them for dismantling.

Forecasts indicate that the global dry bulk carrier fleet will grow by 3.5% in 2026, the fastest annual growth rate since 2020: the Supramax/Handymax fleet will see the largest increase (4.7%), followed by the Panamax/Camsamax fleet (+4.2%), the Handysize fleet (+3.2%), and the VLOC/Capesize fleet (+2.4%).

China’s demand takes center stage

In the demand fundamentals sector, Howe Robinson forecasts that dry bulk trade volume will grow by 1.6% in 2026, remaining largely unchanged from the 1.8% increase in 2025 but falling below the 3.6% growth rate recorded in 2024.

Iron ore demand, accounting for approximately 28% of total dry bulk trade, is expected to grow by 1.7% in 2026, slightly below the 2.1% growth rate in 2025. Coal, the second-largest commodity (24% share), is expected to decline by 1.6%, an improvement from the 4.3% drop in 2025; Grain trade is expected to rebound, growing by 4% this year following a decline in 2025; Bauxite shipments are projected to maintain robust growth at 8.7%, though below the 18.7% surge seen in 2025.

Howe Robinson emphasized China’s role in global ton-mile demand: China’s contribution has begun to wane, while India and Southeast Asia are gaining increasing prominence.

Data indicates that China’s share of annual growth in dry bulk trade ton-miles declined significantly between 2023 and 2025, accounting for only about 34% of the global increase last year. However, Howe Robinson officials stated that demand is expected to rebound in 2026, driven by rising exports of Brazilian iron ore, Guinean iron ore, and bauxite to China.

In 2026, the ton-mile growth rate for the Capesize bulk carrier fleet is projected to reach 2.7%, slightly exceeding the fleet growth forecast of 2.4%. Iron ore accounts for over 70% of the cargo demand, followed by bauxite (16.6%) and coal (9.2%).

Based on current market fundamentals, Howe Robinson anticipates the dry bulk market will peak in the second quarter of 2026.