In the first half of 2026, global orders for alternative-fuel vessels saw a slight slowdown; however, liquefied natural gas (LNG) remained the dominant choice, serving as the preferred fuel type for newbuilds among shipowners.

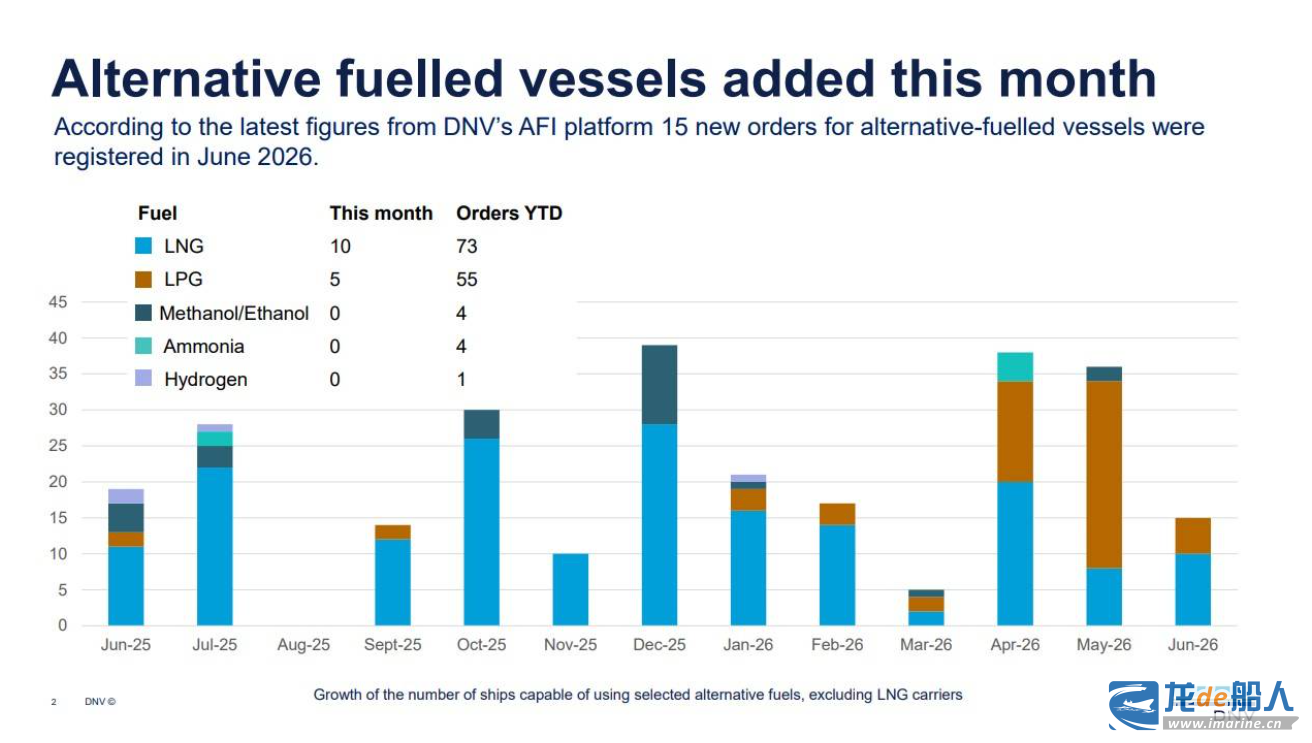

Data from DNV’s Alternative Fuels Insight (AFI) platform indicates that global shipowners placed orders for a total of 137 alternative-fuel vessels during the first half of 2026, a decrease from the 155 vessels ordered during the same period last year. On a monthly basis, 15 vessels were ordered in June, comprising 20 LNG-powered vessels (nine car carriers and one CO2 carrier) and five LPG/ethane-powered vessels; additionally, two LNG bunkering vessels were ordered, bringing the year-to-date total for such vessels to seven.

In terms of fuel type, LNG remains the dominant alternative fuel; of the 137 alternative-fuel vessels ordered in the first half of the year, 73 are LNG-powered. These newbuilds consist primarily of container vessels (42 vessels) and car carriers (21 vessels), reflecting the relatively well-developed LNG bunkering infrastructure and sustained strong demand.

Order momentum for LPG/ethane-powered vessels has strengthened in tandem, with a total of 55 vessels ordered in the first half of the year—a significant increase compared to the 15 vessels ordered during the same period in 2025. Orders for other alternative-fuel vessels included four ammonia-powered vessels, two methanol-powered vessels, two ethanol-powered vessels, and one hydrogen-powered vessel.

Although the growth rate of orders for alternative-fuel vessels has slowed, delivery volumes continue to rise, and the global fleet of such vessels keeps expanding. In the first half of 2026, a total of 61 LNG-powered vessels and 38 methanol-powered vessels entered service.

The first half of the year also saw a milestone for ammonia-powered vessels: Belgian shipowner Exmar took delivery of the world’s first ocean-going ammonia dual-fuel vessel. Unlike previous ammonia-powered demonstration vessels, this vessel will go directly into commercial operation, marking substantial progress toward the large-scale adoption of ammonia as a marine fuel.

Jason Stefanatos, Global Decarbonization Director at DNV Maritime, stated: “The order trends for alternative-fuel vessels in the first half of 2026 demonstrate that market development varies across segments due to differing economic conditions, fuel availability, and regulatory environments; shipowners and other stakeholders are exploring diverse pathways based on their specific priorities and requirements.”

Jason Stefanatos notes that LNG remains the primary short-term fuel choice, driven by demand from the container and car carrier sectors; meanwhile, rising demand for LPG/ethane-powered vessels and continued activity in the ammonia and methanol sectors indicate that the shipping industry has yet to converge on a single, unified decarbonization solution.

Data from the first half of the year illustrates the broader trend of the shipping industry’s energy transition: faced with increasingly stringent regulations and the evolving dynamics of fuel availability, infrastructure, and economics across different trade routes and vessel types, shipowners are not gravitating toward a single alternative fuel but are instead continuing to pursue a diversified investment strategy.