Recently, the shipping brokerage firm BRS Shipbrokers released its “2025 Annual Report.” During the reporting period, global new ship orders in 2025 fell to 176.5 million DWT, down from 196.3 million DWT in 2024.

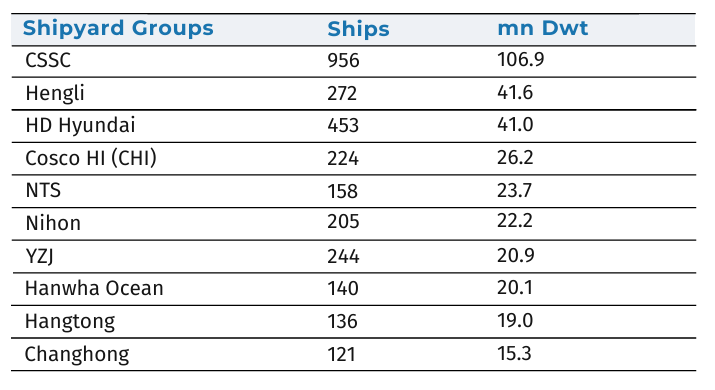

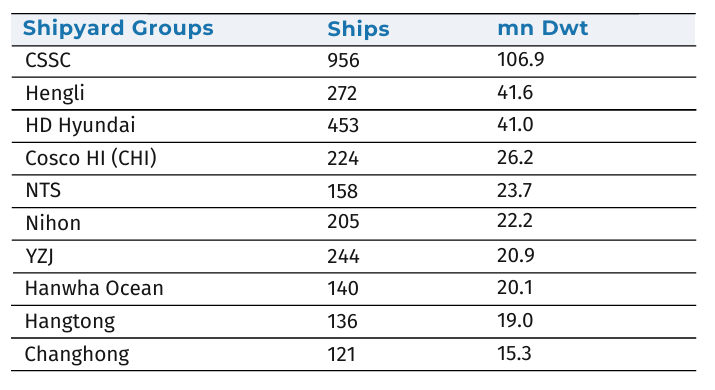

According to data from BRS Shipbrokers, based on order backlog in deadweight tonnage, the top ten shipbuilding groups in 2025 include seven from China, two from South Korea, and one from Japan, as follows:

China State Shipbuilding Corporation (CSSC): With 956 vessels and 106.9 million DWT in order backlog, CSSC firmly holds the top spot globally. Its order backlog accounts for 32.1% of the total orders held by Chinese shipbuilders and 22.7% of the global order backlog. In 2025, CSSC secured new orders totaling 38.9 million DWT, approximately 2.4 times that of South Korea’s largest shipbuilding group, HD Hyundai. Among its subsidiaries, Qingdao Beihai Shipbuilding and Dalian Shipbuilding lead the market in bulk carrier and tanker orders, respectively.

Hengli Heavy Industries: With a backlog of 272 vessels totaling 41.6 million DWT, it ranks second globally. Its backlog accounts for 12.5% of the total orders held by Chinese shipbuilders and 8.8% of the global total. In terms of deliveries, Hengli Heavy Industries delivered only 4 vessels in 2024 and is scheduled to deliver 17 in 2025. It is currently China’s second-largest builder of bulk carriers and oil tankers.

HD Hyundai: With a book order volume of 453 vessels and 41 million DWT, it ranks third globally. Its shipyards include HD Hyundai Heavy Industries (including HD Hyundai Mipo, which will be merged by the end of 2025) and HD Hyundai Samho. Its book order volume accounts for 43.8% of the total orders held by South Korean shipbuilders.

COSCO Shipping Heavy Industry (including Nantong COSCO Shipping Kawasaki and Dalian COSCO Shipping Kawasaki): With a book order volume of 224 vessels and 26.2 million DWT, it ranks fourth globally. Its book order volume accounts for 7.9% of the total orders held by Chinese shipbuilders and 5.6% of the global total. In 2025, COSCO Shipping Heavy Industry secured a total of 8.4 million DWT in new ship orders, accounting for approximately 4.8% of the global total.

New Era Shipbuilding: With a book order volume of 158 vessels and 23.7 million DWT, it ranks fifth globally, up from seventh in 2024. Its book order volume accounts for 7.1% of the total orders of Chinese shipbuilders and 5% of the global total, demonstrating strong performance in tanker and container ship orders. In 2025, New Era Shipbuilding secured a total of 3.8 million DWT in new ship orders, accounting for approximately 2.2% of the global total.

Nihon Shipyard: With 205 vessels and 22.2 million DWT in its order book, it ranks sixth globally. In 2025, Nihon Shipyard’s order intake slowed significantly, securing contracts for only 28 new vessels—far below the 130 vessels in 2023 and 88 vessels in 2024.

Yangzijiang Shipbuilding: With a book order volume of 244 vessels and 20.9 million DWT, it ranks seventh globally. Its book order volume accounts for 6.3% of the total orders of Chinese shipbuilders and 4.4% of the global total.

Hanwha Ocean: With 140 vessels and 20.1 million DWT in its order book, it ranks eighth globally.

Hantong Shipbuilding: With 136 vessels and 19 million DWT in its order book, it ranks ninth globally.

Zhoushan Changhong International: With 121 vessels and 15.3 million DWT in its order book, it ranks tenth globally.

In 2025, the combined order backlog of China’s five major shipbuilding groups—China State Shipbuilding Corporation, Hengli Heavy Industry, COSCO Shipping Heavy Industry, New Era Shipbuilding, and Yangzijiang Shipbuilding—accounted for 65.8% of the total order backlog held by Chinese shipbuilders, reaching 219.3 million DWT; their share of the global order backlog remained unchanged from 2024, at 46.6%.

Notably, during the statistical period covered by BRS Shipbrokers, Samsung Heavy Industries—one of South Korea’s three major shipbuilding giants—did not make the list of the world’s top ten shipbuilding groups in 2025. Another significant feature of this list is the rising market share of China’s private shipbuilding enterprises, reflecting their remarkable growth.

According to BRS Shipbrokers’ annual report, as of the end of 2025, tanker orders stood at 52.2 million DWT, marking the first decline since the post-COVID-19 rebound and a 19% year-on-year decrease (from 64.2 million DWT), though still 75% higher than the ten-year average. Bulk carrier orders stood at 53.6 million DWT, down 11% year-over-year (from 59.9 million DWT), yet still 34% higher than the ten-year average; in contrast, container ship orders reached 60.1 million DWT, up 18% year-over-year (from 50.9 million DWT), marking the highest and most stable order level on record.

In 2025, Chinese shipbuilders continued to lead the markets for bulk carriers, container ships, and oil tankers, ranking first with 45.3 million DWT and an 84.5% market share, 46.4 million DWT and a 77.2% market share, and 31.1 million DWT and a 59.6% market share, respectively. In other segments, they collectively held the top position with 4.8 million DWT and a 45.4% market share.

In terms of shipbuilding capacity, by the end of 2025, the total capacity of Chinese shipbuilders reached 53 million DWT, a 10.5% increase year-on-year (up from 48 million DWT). The ratio of order backlog to annual capacity stood at 6.3, setting a new record high compared to 5.4 in 2024 and 3.7 in 2023. This indicates that most Chinese shipyards are fully booked for the next three to four years, with virtually no available delivery slots until 2029.

Although global new ship orders have declined year-on-year, Chinese shipbuilders have maintained a robust market share, continuing to consolidate their dominant position in the new shipbuilding market.