Data from shipping consultancy Veson Nautical indicates that over the past year, China’s shipbuilding industry has maintained its dominant position in global new ship orders. Chinese shipbuilders have further solidified their strong competitiveness in the worldwide newbuilding market, securing new orders across key vessel types including Very Large Crude Carriers (VLCCs), liquefied natural gas (LNG) carriers, container ships, and bulk carriers.

The list of shipbuilders includes: Hudong-Zhonghua Shipbuilding, Hengli Heavy Industries, New Times Shipbuilding, Qingdao Beihai Shipbuilding, Wuhu Shipyard, Fujian Mawei Shipbuilding, Zhoushan Changhong International, Huangpu Wenchong Shipbuilding, Dalian Shipbuilding Industry Corporation (DSIC), and New Hantong Ship Heavy Industry Co., Ltd (NHT).

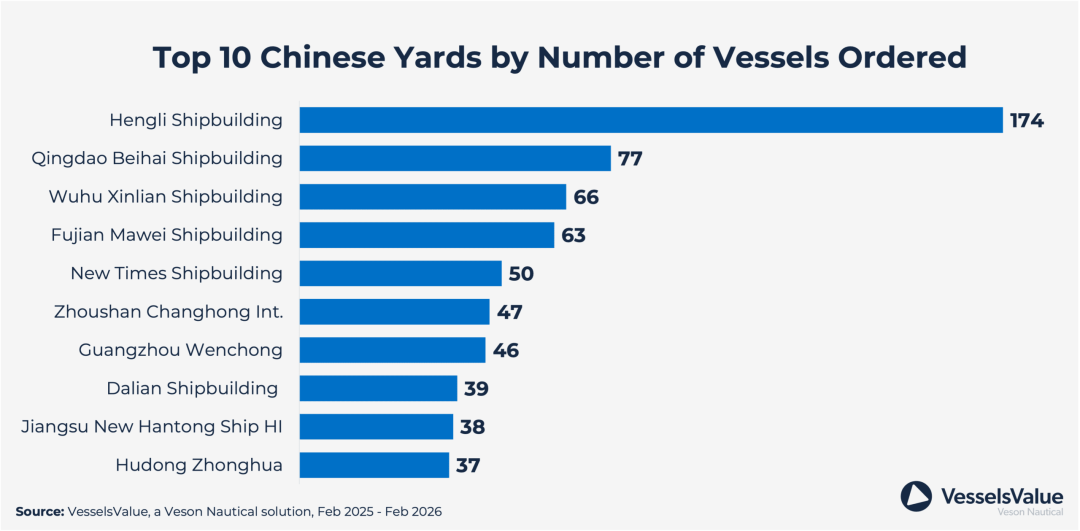

Based on the number of new ship orders secured, the top ten Chinese shipbuilders during the statistical period (February 2025 to February 2026) are ranked as follows:

- Hengli Heavy Industries tops the list with 174 vessels on order. Hengli Heavy Industries commenced full-scale production in 2023. Formerly known as STX (Dalian) Shipbuilding, it is a relatively young shipbuilder. Its primary vessel types include VLCCs, accounting for 31% of orders; LR2 product tankers rank second at 15%; and Post-Panamax container ships rank third at 12%.

- Qingdao Beihai Shipbuilding ranked second with 77 vessels. The orders are heavily concentrated on Capesize bulk carriers. Among the 49 210,000 DWT Newcastlemax bulk carriers ordered by COSCO Shipping Bulk, 31 are being built by Beihai Shipbuilding, with deliveries scheduled between 2027 and 2031.

- Wuhu Shipyard ranked third with 66 vessels in its orderbook. The most popular vessel types at this shipyard are Ultramax bulk carriers and Handy bulk carriers, accounting for 31% and 15% of the total orders respectively.

- Fujian Mawei Shipbuilding ranked fourth with 63 vessels ordered. Its orders primarily consist of Panamax bulk carriers and Handy container ships, accounting for 46% and 37% of its order portfolio respectively.

- New Times Shipbuilding ranked fifth with 50 vessels;

- Zhoushan Changhong International ranked sixth with 47 vessels;

- Huangpu Wenchong ranked seventh with 46 vessels ordered;

- DSIC ranks eighth with 39 vessels ordered;

- NHT ranked ninth with 38 vessels ordered;

- Hudong-Zhonghua Shipbuilding ranks tenth with 37 vessels ordered.

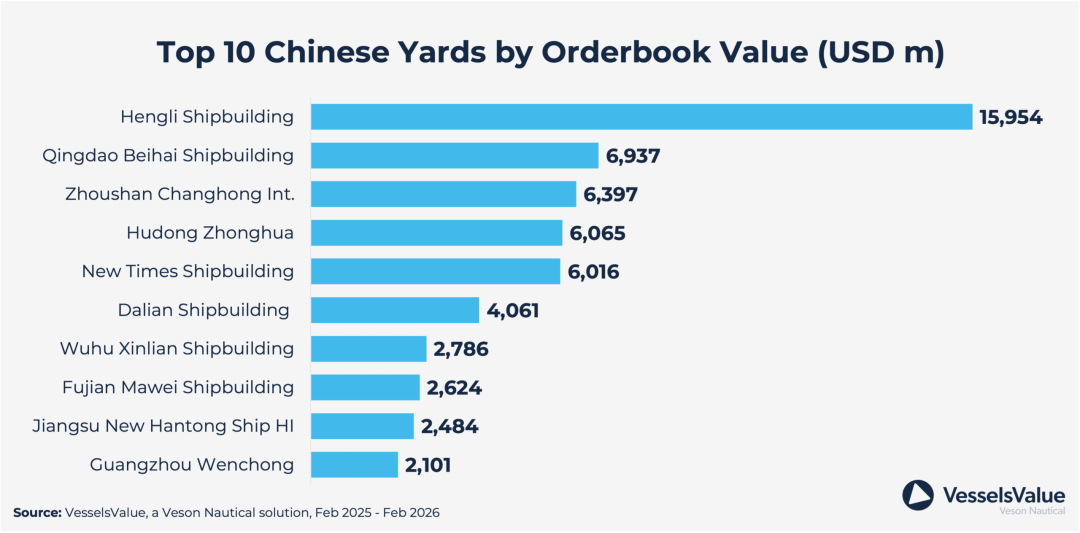

Based on order value, the top ten Chinese shipbuilders during the statistical period (February 2025 to February 2026) are ranked as follows:

- Hengli Heavy Industries topped the list with an order value of approximately $15.954 billion;

- Qingdao Beihai Shipbuilding ranked second with an order value of approximately $6.937 billion;

- Zhoushan Changhong International came in third with an order value of approximately $6.397 billion;

- Hudong-Zhonghua Shipbuilding ranked fourth with an order value of approximately $6.065 billion. This ranking differs significantly from the order volume-based list, where it placed tenth, primarily due to Hudong-Zhonghua’s substantial intake of high-value-added vessel types: LNG carriers accounted for 35% of its order volume;

- New Times Shipbuilding ranked fifth with approximately $6.015 billion in order value;

- DSIC ranked sixth with approximately $4.061 billion in order value;

- Wuhu Shipyard ranked seventh with an order value of approximately $2.786 billion;

- Fujian Mawei Shipbuilding ranked eighth with an order value of approximately $2.624 billion;

- NHT ranked ninth with an order value of approximately $2.484 billion;

Huangpu Wenchong ranked tenth with an order value of approximately $2.101 billion.

Currently, China’s leading shipbuilders are accelerating their operations, with some shipbuilders having order backlogs extending into the latter part of this decade. The value of these orders reflects the continued strong market demand for multiple vessel types.

The rapid rise of Hengli Heavy Industries, Hudong-Zhonghua’s portfolio of high-value-added orders, and the extensive business footprints of other shipbuilders indicate that China’s shipbuilding industry is currently operating at full capacity with no signs of slowing down.