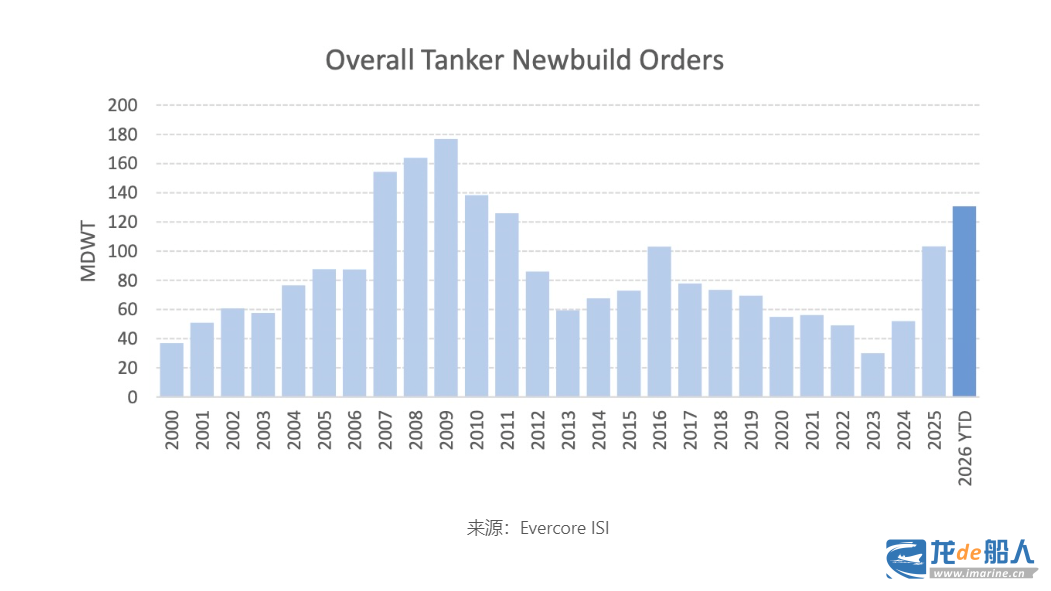

The tanker industry is poised for a surge in capacity, with the latest research indicating that new tanker orders in 2026 are expected to reach a record high. Investment bank Evercore ISI points out that the total number of tanker orders in the first four and a half months of 2026 already ranks as the fifth highest this century.

Becky Smart, a research analyst at Singapore-based shipbroker Sentosa Shipbrokers, said: “The tanker market is currently facing a real risk of overcapacity. The tanker fleet is projected to grow by 11% by deadweight tonnage by the end of 2027, far exceeding the latest oil demand growth figure of 1%-2% for the same period. The longer the situation in the Strait of Hormuz continues, the more severe this supply-demand gap will become, thereby suppressing oil demand growth and triggering a wider economic ripple effect.”

Becky Smart also emphasized: “The actual situation is more complex. The tanker market is performing strongly in an inefficient operating environment, which may absorb a large amount of new capacity. On paper, oversupply is almost a certainty, but considering the realities of the tanker market, geopolitics, sanctions, fleet aging, and changes in trade flows, the amount of new capacity that the market can absorb before freight rates are impacted may exceed expectations.”

Breakwave Advisors analysts warned in a recent report that the recent orders for multiple oil tankers will lead to “a significant long-term supply-demand imbalance, potentially triggering a downturn.”

In contrast, Ralph Leszczynski, head of research at shipbroker Banchero Costa, believes that the risk of overcapacity from this wave of tanker orders may not be as severe as expected. He explains that 20 to 25 years have passed since the last large-scale fleet replacement driven by legislation requiring the elimination of single-hull tankers. This means that many currently operating tankers are now 20-25 years old and naturally entering their scrapping and replacement cycle.

Furthermore, a large number of oil tankers that should have been scrapped long ago continue to operate in the “shadow trade” in places like Russia, Iran, and Venezuela. However, most of these vessels are old and poorly maintained, making it impossible for them to return to compliant mainstream trade. Therefore, once the reasons for the existence of such “shadow trade” disappear, most of these vessels will be forced to be scrapped, and they will be replaced by a modern and compliant fleet.

Furthermore, a large number of oil tankers that should have been scrapped long ago continue to operate in the “shadow trade” in places like Russia, Iran, and Venezuela. However, most of these vessels are old and poorly maintained, making it impossible for them to return to compliant mainstream trade. Therefore, once the reasons for the existence of such “shadow trade” disappear, most of these vessels will be forced to be scrapped, and they will be replaced by a modern and compliant fleet.

Currently, tanker freight rates are at unprecedented highs. Alex Saverys, CEO of CMB.TECH, one of Europe’s largest shipowners, said when announcing the first quarter results for 2026: “The tanker market is currently ‘extremely hot.’ With many uncertainties in global trade and a continuous increase in new ship orders, the market cannot predict how long this ‘golden window’ can last.”